How to automate customer risk analysis in B2B thanks to AI

In a B2B world where financing, partnership or insurance decisions depend on a rapid but reliable analysis of customer risk, the ability to automate this process becomes a major competitive advantage.

Historically, this analysis relied on manual tools, Excel spreadsheets and human expertise that was sometimes biased or outdated. But today, thanks to artificial intelligence (AI) technologies, it is possible to assess credit or compliance risk in a matter of seconds, with a high level of accuracy and traceability.

In this article, we'll show you why automated customer risk analysis has become a must in B2B, how it works in practice, and how to avoid common mistakes when implementing it.

Manual vs. automated analysis: a concrete comparison

🔧 The traditional process

In many B2B structures, customer risk analysis is still largely a manual process:

- Collection of financial documents (balance sheets, income statements), legal documents (Kbis, articles of association), administrative documents (SIREN, Banque de France listing)

- Data entry or review in Excel or CRM

- Application of internal rating grids that are often obsolete

- Human decision, sometimes subjective, with little documented justification

This type of scoring has a number of disadvantages:

- High processing times (up to 1h/file)

- Quality varies by analyst

- Limited traceability

- Low scalability

⚙️ The automated process with AI

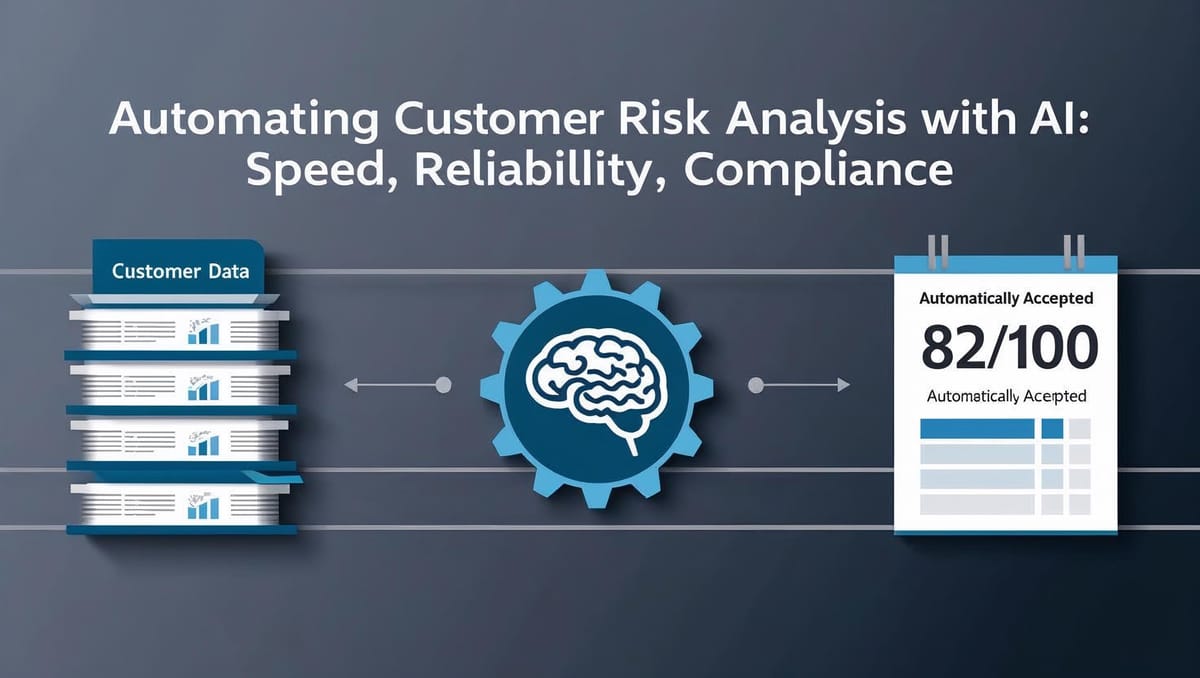

With a solution like RocketFin, scoring is automated from start to finish:

- Automatic data collection via API (Infogreffe, Insee, partner banks, third-party suppliers)

- Data cross-analysis by an AI engine trained on thousands of cases

- Scoring objective (e.g. 78/100) based on :

- Financial data (liquidity, EBITDA, cash flow)

- Behavioral data (late payments, collections)

- Legal and industry data

- Detection of anomalies (e.g. inactive SIREN, discrepancy between status and actual activity)

- Immediate decision or awaiting human validation

Concrete benefits of B2B automated scoring

✅ 1. reliability & consistency

The criteria are applied without any variation in interpretation, unlike human assessments.

📌 Example: two identical startups will no longer be rated differently depending on the analyst.

⚡ 2. Processing speed

The full score is generated in less than 5 seconds, even with cross-checks on several bases.

⚙️ Considerable productivity gains, especially for platforms handling several dozen files a day.

🛡️ 3. Enhanced compliance

AI can natively integrate :

- LCB-FT rules

- KYC and beneficiary checks

- RGPD vigilance thresholds (e.g. exclusion of sensitive criteria)

🧠 RocketFin offers a complete audit trail for every decision.

🧩 4. Sector adaptability

Business rules can be calibrated by sector:

- Horeca = strong seasonality

- SaaS = importance of recurring revenues

- BTP = dependence on deferred invoicing

What AI doesn't replace (yet)

Although powerful, AI must not operate in a vacuum.

Cases requiring human intervention :

- Files with intermediate scores (between 50 and 70)

- Presence of contradictory indicators (e.g. good EBITDA but SIREN inactive)

- Cases of fraud or attempted concealment

RocketFin allows a hybrid mode, in which certain cases are automatically "escalated" to manual validation.

📊 Concrete examples: from theory to practice

🏢 Case #1: Fast-growing tech start-up

- Sales up, but little profit

- Balance sheet limited to 2 financial years

- Application rejected by a traditional bank

Result with RocketFin:

Score 79/100 thanks to recurring revenue analysis + perfect compliance → Automated acceptance

🛠️ Case #2: Industrial SME with anomalies

- SIREN valid but inactive according to Insee

- Recent status does not correspond to declared activity

- Frequent delays in supplier payments

RocketFin result:

Score 42/100 + legal inconsistency alert → File marked "for manual validation".

✅ Best practices for automating risk analysis

- Connect your data sources (banks, accounting, legaltech)

- Définir vos seuils de confiance (ex : > 70 = accepté, < 50 = refusé)

- Test the tool on old files already scored manually

- Combining AI + human analysis in one clear workflow

- Train your team in the scoring engine's criteria

❌ Common mistakes to avoid

- Underestimate the biases of human scoring (overconfidence, halo effect)

- Apply the same criteria to all sectors

- Using AI without initial verification

- No feedback loop to improve the model

FAQ - B2B customer risk automation

What types of data are analyzed?

Financial, legal, behavioral, banking, sectoral.

Is automation RGPD-compatible?

Yes, as long as it does not integrate sensitive data, offers an explanation of decisions and includes a right to human review.

Can the scoring engine be customized?

Yes, RocketFin lets you configure specific rules according to sector, strategy or tolerated risk level.

🔗 Read more

👉 Discover how RocketFin automates B2B credit scoring in real time: www.rocketfin.ai

🟢 Would you like to test RocketFin in advance?

Request your access here